The $230 Billion Biologics Patent Cliff

What stands out to me about the biologics patent cliff is its scale. For years, biologics were among the best businesses in pharma. These complex drugs, often made from living cells, became huge sellers in cancer, autoimmune disease, and inflammatory disorders. They were hard to manufacture, hard to copy, and protected by patents for years. That gave them unusual staying power.

Now that protection is weakening. According to IQVIA, a healthcare analytics company that tracks drug markets and industry trends, 118 biologics are expected to lose patent protection in the United States from 2025 through 2034. Together, they represent a biosimilar opportunity worth more than $230 billion.

On paper, the story looks simple. Patents expire. Biosimilars arrive. Prices fall. Treatment gets cheaper. Some of this is already happening. HHS says biosimilars have generated $56 billion in healthcare savings since 2015, with $20 billion of that in 2024 alone. It also says the average biosimilar launches at about half the price of the original biologic.

The problem is timing. Patent loss and real competition are moving on different schedules. IQVIA found that only 12 of those 118 biologics had biosimilars in development as of June 2024. So the number of drugs approaching patent expiration is far larger than the number of competitors now on the way.

You can already see how uneven this transition is. Johnson & Johnson’s Stelara, used for inflammatory diseases such as psoriasis, Crohn’s disease, and ulcerative colitis, lost ground quickly after biosimilar entry, with sales falling about 60 percent. AbbVie’s Humira, which treats many similar inflammatory disorders, followed a very different path. Even after nine biosimilars entered the U.S. market, Humira still held on to more than 80 percent of patients. These two drugs operate in closely overlapping markets, yet they responded very differently to biosimilar pressure.

What the Biologics Patent Cliff Really Means

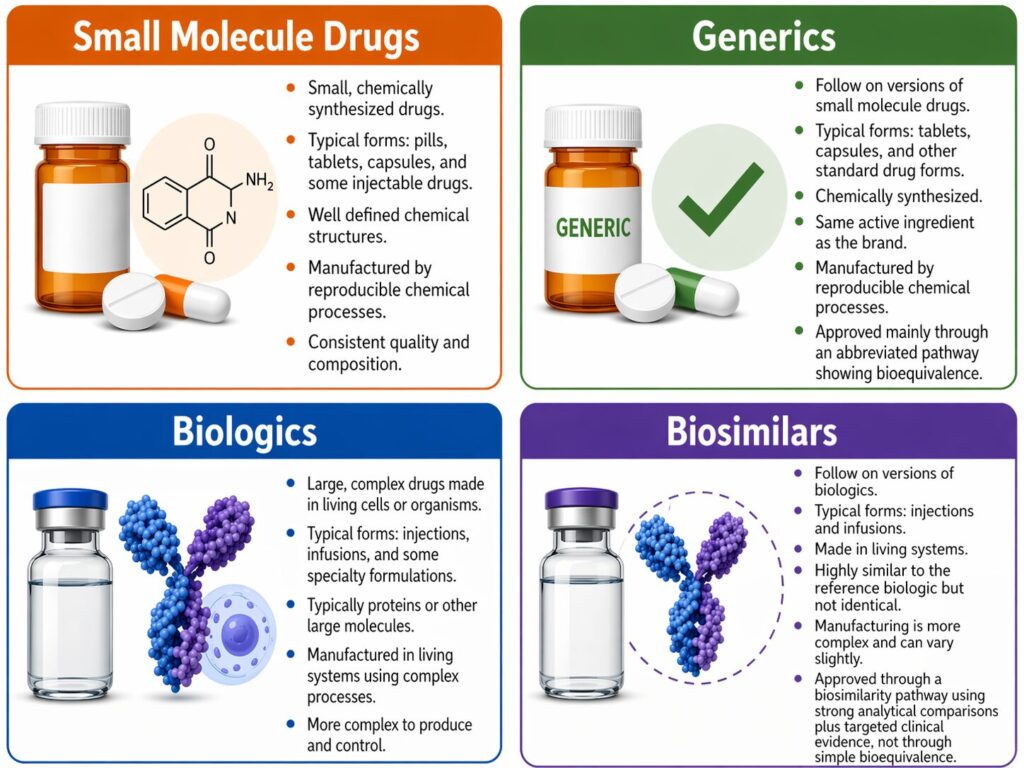

A patent cliff begins when a blockbuster drug loses exclusivity and starts losing revenue. With ordinary drugs, this can happen fast. Generic versions appear. Prices drop. The original brand loses sales.

The biologics patent cliff follows the same broad logic, but the process is slower and rougher. Biologics are larger and more complex than standard pills. Companies make them from living cells. So they do not produce exact generic copies. They produce biosimilars, which must be shown to be highly similar to the original drug.

That difference shapes the whole market. Generic drugs can take share quickly. Biosimilars enter a harder environment. Manufacturing is tougher. Patent disputes can drag on. Insurance coverage and rebate deals shape prescribing. Doctors may also hesitate to switch patients who are stable on the original drug.

Why the Biologics Patent Cliff Is Hitting Now

The timing is no accident. It reflects the history of modern biotech. Over the past few decades, biologics moved from a specialized corner of medicine into the center of the pharmaceutical business. Therapeutic antibodies drove much of this shift. They became one of the industry’s biggest success stories, and they rose within a fairly concentrated historical window.

That created a cohort effect. A whole generation of blockbuster biologics entered the market within the same broad stretch of time. These drugs then enjoyed long periods of patent protection and exclusivity. Now many are nearing the end of that cycle together.

The pattern runs across several branches of medicine. Humira and Stelara, for example, both became giant biologics in overlapping inflammatory disease markets and have now entered the loss of exclusivity phase. Eylea, a retinal disease drug used for wet age related macular degeneration and related eye conditions, has also entered that phase, with biosimilars approved and at least one already launched in the U.S. Keytruda, Merck’s cancer immunotherapy, represents the next phase of the same patent wave, with key patents beginning to expire in 2028.

This is why the biologics patent cliff feels so large. A whole generation of blockbuster biologics is reaching this point at roughly the same time.

Why Competition Is Arriving Unevenly in the Biologics Patent Cliff

The biologics patent cliff is not unfolding smoothly. Biosimilars have become easier to develop, but that does not mean they are easy. The FDA has tried to streamline the process by putting more weight on detailed lab comparisons between a biosimilar and the original drug, rather than requiring as much animal testing and as many large clinical comparison trials as companies once expected. Strong analytical data can reduce the need for some slower and more expensive follow up studies.

Even so, the barriers remain substantial. Biologics are still hard to manufacture, expensive to develop, and uncertain in their economics. IQVIA found that only about 10 percent of the biologics expected to lose patent protection from 2025 through 2034 currently have biosimilars in development. Most of that activity is concentrated in the drugs with the biggest sales and the nearest patent expirations.

Then there is the market itself. Humira and Stelara show how uneven the biologics patent cliff can be even within closely overlapping inflammatory disease markets. Humira held on to more than 80 percent of patients even after nine biosimilars entered the U.S. market. Stelara, by contrast, lost ground much faster after biosimilar entry.

Therapeutic area alone does not explain that difference. Humira appears to have benefited from stronger market defense. AbbVie secured favorable formulary placement, used aggressive rebate contracting, and faced slower switching by pharmacy benefit managers and insurers. Few patients moved to a Humira biosimilar until major coverage decisions started to change. Stelara seems to have faced a different competitive dynamic, with some patients moving not only to Stelara biosimilars but also to other treatments such as Tremfya.

So the problem in the biologics patent cliff is not simply biosimilar development. Even after they reach the market, they still have to fight through the market itself.

Why the Biologics Patent Cliff Is Driving a Big Pharma Race for Innovation

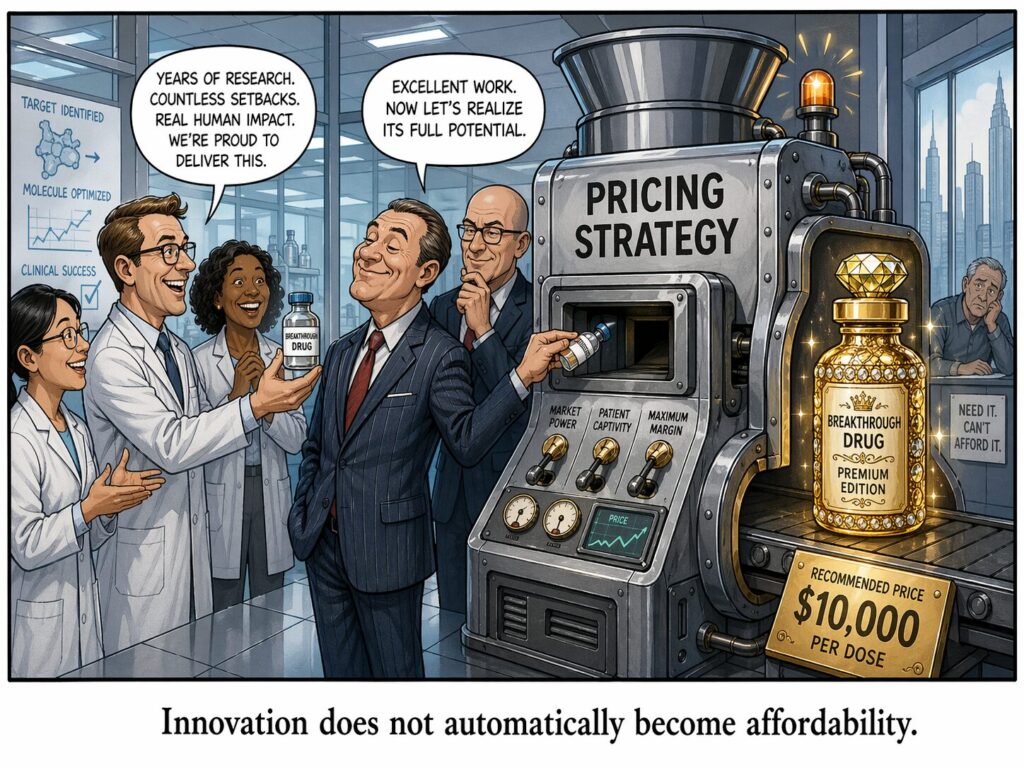

For big pharma, an approaching loss of exclusivity becomes urgent long before a patent expires. Once a company can see the date on the horizon, the issue turns into a revenue problem.

Merck is a case in point. In February 2026, Reuters reported that the company was reorganizing around Keytruda as key patents moved toward expiration in 2028. Keytruda brought in more than $30 billion in 2025 and accounted for nearly half of Merck’s total revenue. A company in this position does not sit still and hope for the best.

That helps explain the scramble for deals. Reuters reported in March 2026 that looming patent loss was pushing many large drugmakers toward late stage or otherwise de risked biotech assets that could be folded quickly into existing development and commercial systems. Around the same time, drugmakers were leaning harder on licensing deals, including deals for assets coming out of China, as they searched for outside programs to replace aging revenue streams.

The same pressure shows up in individual transactions. Novartis bought Anthos Therapeutics in 2025 to strengthen its cardiovascular business as Entresto, its heart failure drug, moved toward patent expiry. Gilead negotiated to buy Ouro Medicines in 2026, gaining access to an experimental antibody for autoimmune diseases as it tried to strengthen its immunology pipeline.

These moves tell us something about the big pharma race for innovation. Companies are looking for assets with enough novelty and strategic value to become major franchises of their own. In the best case, that pressure pushes pharma toward better therapies. But there is no guarantee. A harsher innovation race can produce real breakthroughs, but it can also produce very expensive drugs whose advantages are less dramatic than their price tags suggest.

What the Biologics Patent Cliff Could Mean for Biosimilars and Drug Prices

Patients could still be the biggest winners from the biologics patent cliff. Biosimilars have already generated substantial savings, and broader adoption should lower costs for some of the most expensive drugs in medicine.

But lower prices do not automatically reach patients. Savings depend on more than the science behind a biosimilar. They depend on patent rules, rebate arrangements, pharmacy benefit managers, insurer formularies, and how willing doctors and health systems are to switch patients. The FDA can lower barriers to entry, but it cannot force savings to move quickly through a market built to slow change.

So yes, the biologics patent cliff could bring cheaper treatment. However, whether it does will depend on whether competition can break through those market barriers.

The Biologics Patent Cliff and the End of the Old Blockbuster Model

The older blockbuster model is still alive, but it is starting to look less stable.

For a long time, a small number of protected drugs could carry a large share of a company’s revenue. Merck’s dependence on Keytruda shows one side of the problem. Johnson & Johnson’s drop in Stelara after biosimilar entry shows the other. One company is approaching the cliff. Another is already living below it.

What is weakening is an older assumption that a handful of giant franchises can provide years of relative stability. IQVIA’s numbers point in the same direction. A large wave of biologics is due to lose patent protection over the next decade, yet only a small fraction currently have biosimilars in development. Old monopolies are weakening. The replacement market is still being built.

This shift reaches beyond pricing. It changes how large drug companies think about survival. The older model relied on a few massive protected products. The next model will rely more on constant renewal, stronger pipelines, and assets that can stand out in a tougher market. The blockbuster era is not ending overnight. Still, the ground under it is moving.

Conclusion: The Biologics Patent Cliff Is Underway, but the Outcome Is Still Open

A large generation of biologic blockbusters is moving toward loss of patent protection, and this will change pharma whether the industry is ready or not. But patents alone will not decide what happens next. The real question is whether biosimilar competition can push through the market structures that still protect old blockbusters.

Patients could still come out ahead. Big pharma’s scramble for replacement winners could also produce better drugs. But neither outcome is automatic. The biologics patent cliff is real. Whether it brings cheaper treatment, stronger innovation, or simply a reshuffled version of the old order is still an open question.

Your Thoughts

What do you think?

Will the biologics patent cliff really lower drug prices, or will market barriers keep many of those savings from reaching patients? Do you think big pharma’s scramble for new winners will lead to better drugs, or just more expensive ones?

And which side of the story strikes you as more important: the promise of biosimilars, or the way companies like AbbVie have managed to defend market share even after competition arrived?

I’d love to hear your thoughts in the comments.

Bleeding Edge Biology Recommends

Articles

- Revisiting Expectations of US Biosimilars—Panacea or One Piece of the Puzzle? — Andrew W. Mulcahy, JAMA Health Forum, March 1, 2024

Readers looking for a clear reality check on biosimilars will find it here. The article asks whether biosimilars can really lower drug costs on their own, or whether they are only one part of a much larger policy problem. - Biologic Drug Prices in Medicare Part B After Entry of Biosimilars to the Market — Abdullah Abdelaziz, Aaron N. Winn, Stacie B. Dusetzina, and Aaron P. Mitchell, JAMA Network Open, November 11, 2025

Readers who want hard numbers rather than general claims should start here. This study looks at what actually happened to biologic drug prices after biosimilars entered Medicare Part B, and shows that the savings are real but not always dramatic. - Clearing Dense Drug-Patent Thickets — Bernard Chao, Ryan Whalen, Aaron S. Kesselheim, and S. Sean Tu, The New England Journal of Medicine, December 12, 2024

This article is especially useful for readers who want to understand why competition often arrives later than it should. It focuses on the dense patent webs that can delay generic and biosimilar entry long after a drug’s original protection was supposed to weaken. - FDA’s Regulatory Reforms to Unlock Competition and Lower Drug Costs: Breaking the Biosimilar Bottleneck — Martin A. Makary, Sarah Yim, Mustafa Ünlü, and M. Stacey Ricci, JAMA, 2025

Readers interested in the regulator’s side of the story will find this especially helpful. It lays out where FDA officials think the bottlenecks are and why newer reforms might make biosimilar development faster and cheaper.

Talks

- Why are drug prices so high? Investigating the outdated US patent system — Priti Krishtel, TED, January 2020

This is a strong entry point for readers who want a broad public facing explanation of why drug prices stay so high. It widens the frame beyond biosimilars and shows how patent rules help shape the entire system. - Changing the drug pricing game — Peter Bach, TEDMED, 2017

Readers who want the pricing debate in plain English will get a lot out of this talk. Bach explains the incentives behind high drug prices without oversimplifying the problem. - 3 reasons why medications are so expensive in the US — Kiah Williams, TED-Ed, October 24, 2024

This is a useful primer for readers who are newer to the subject. It gives a simple map of the U.S. drug pricing system before they move on to the more specialized questions around biologics and biosimilars.

Documentaries

- The Other Drug War — Directed by Jon Palfreman and Barbara Moran, FRONTLINE/PBS, June 19, 2003

Even though it is older, this documentary still works well as background. Readers interested in the larger political fight over prescription drug prices will find that many of its core tensions are still with us. - Cracking the Code: Phil Sharp and the Biotech Revolution — Directed by Bill Haney, Independent Lens/PBS, 2025

This is a good pick for readers who want to step back from biosimilars and look at the broader rise of biotechnology. It helps place today’s blockbuster biologics in the longer history of the biotech industry.

Websites and Reports

- Assessing the Biosimilar Void in the U.S. — IQVIA Institute, February 3, 2025

Readers who want the core market data behind this post should start here. This report lays out the mismatch between the large number of biologics approaching patent loss and the much smaller number of biosimilars actually in development. - Biosimilars — U.S. Food and Drug Administration, current page dated March 1, 2023

This is the best official starting point for readers who want to understand what biosimilars are and how the FDA evaluates them. It is especially useful for anyone who still thinks biosimilars are just generic drugs under another name. - Competition in the U.S. Therapeutic Biologics Market — Office of the Assistant Secretary for Planning and Evaluation, U.S. Department of Health and Human Services, July 2, 2025

Readers who want the policy angle will find this report useful. It focuses on how limited biosimilar competition still is in the U.S. biologics market and helps explain why lower prices do not automatically follow from patent expiration.